Emerging MEMS sensors, significant cost reductions, increasing importance of software and new technologies, and the rise of industry giants and Chinese foundries: In 2020, the global MEMS industry will exceed $20 billion! Traffic Facilities,Waterproof Traffic Facilities,Outdoor Traffic Facilities,Traffic Control Devices Yangzhou Heli Photoelectric Co., Ltd. , https://www.heli-eee.com

The MEMS industry is more and more mature, emerging devices are emerging

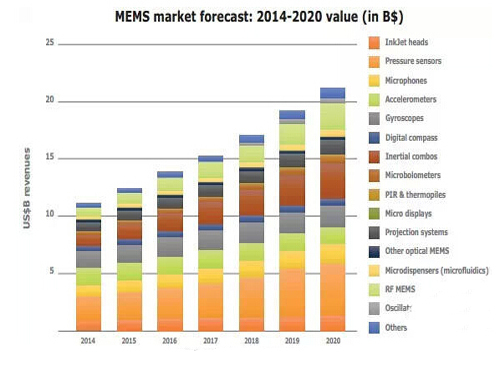

In 2014, the market size of silicon-based MEMS devices reached 11.1 billion U.S. dollars. Due to the huge market demand for smart phones and tablets, the development of the MEMS industry has entered the fast lane, followed by the wearable and Internet of Things (IoT) market driven by unlimited growth potential. At the same time, the MEMS industry is also highly dynamic. Even a more mature automotive market requires new technologies to challenge the existing landscape. Some MEMS devices cost only a few tens of cents to manufacture. For example, motion sensors are becoming a cheap commodity, just like temperature sensors a few years ago. The mature process meets the demand for larger market capacity and the integration of multiple sensor systems, which also prompts MEMS manufacturing to quickly shift to the next generation wafer size.

In addition, we believe emerging MEMS devices continue to emerge. Although gas and chemical sensors are based on semiconductor technology, MEMS technology can further reduce size and cost, opening up new opportunities. We believe that MEMS-based gas sensors will gain more and more applications, especially wearable and consumer electronics devices such as smart phones and smart glasses. Another example is that MEMS micromirrors are attracting attention from the optical communications market, such as the rapid growth of the Calient; or MEMS micromirrors applied to human-computer interaction interfaces, such as Intel's acquisition of Lemoptix.

In the past, we have seen leaders in different markets and the competition is open. But what is still fresh in 2014 is the growth of a future MEMS giant, Robert Bosch. Last year, due to the consumer market, the company's MEMS revenue increased by 20% to reach 1.2 billion US dollars, ranking first in the world. STMicroelectronics’ MEMS revenue now lags behind Bosch’s $400 million. Compared to 2013, the world’s top five MEMS companies have not changed, with total revenues of US$3.8 billion, accounting for about one-third of the global MEMS market. Bosch’s dominance is obvious because it accounts for about one-third of the total revenue of the top five companies.

MEMS has always relied on the use of semiconductor-based microfabrication techniques to fabricate devices to replace more complex, cumbersome, or insensitive sensors. Our analysis shows that there are four trends that will change the MEMS market structure in the future:

Emerging devices such as gas sensors, micromirrors and environmental sensors

New applications such as pressure sensor for position (height) sensing

Disruptive technologies, including packaging, new materials (such as piezoelectric films and 300mm/12-inch wafers)

New designs, including NEMS (electromechanical systems) and optical integration technology

The MEMS market shuffles the old fashioned giants to the newest seniors

The top ten MEMS manufacturers in the world occupy most of the market share. We divide them into two categories: “a strong and aggressive player†and “a struggling giant.†"The aggressive players" include Bosch, InvenSense, Avago and Qorvo. Bosch deserves special attention because it is currently the only dual-market (automotive and consumer electronics) MEMS company in the top 30, and also has dual facilities for R&D and mass production. "Struggling giants" include STMicroelectronics, HP, Texas Instruments, Canon, Knowles Electronics, Denso and Panasonic. These companies are currently trying to find an effective growth engine. In addition, it is worth mentioning that some "little giants" such as Qorvo and Infineon have the potential to develop into "big players" or "giants" in the future.

This report will analyze the MEMS business development of the top 30 MEMS manufacturers worldwide, including MEMS product lines and system integration products. The development direction of MEMS companies: (1) The development of a single MEMS product line into a diversified product line; (2) The development of a MEMS product line as a system integration product line. So far, Bosch is the most successful case.

Future Opportunities: Software, 12-inch wafers, new inspection methods, and emerging sensors

12-inch MEMS wafer fabrication will become a hot topic in the coming years. The 12-inch wafer fabrication will affect the entire MEMS supply chain, including design, materials, equipment, and packaging. Currently, there are two main reasons driving 12-inch wafer fabrication:

(1) Technical requirements, such as devices with CMOS layers are expected to have smaller feature sizes, and wafer size expansion and chip feature size reduction are correspondingly promoted and mutually promoted. Wafer size will increase with each level increase. The feature size of the chip is reduced by one level;

(2) Economic needs: The company pursues continuous reduction of costs and increase of production.

Packaging has become the focus of many MEMS companies, but now software is becoming an important part of MEMS sensors. With the further integration of sensors, more and more data needs to be processed, and software makes multiple data fusion possible. As the importance of software has become increasingly prominent, acquisitions continue to occur, as InvenSense acquired Movea.

With the development of NEMS, new packaging technology and other factors, a new round of MEMS investment cycle begins.

Although the market for combination sensors continues to grow, there are still bright spots in the discrete inertial sensor market.

From 2015 to 2020, consumer applications will continue to grow significantly. It is expected that the annual growth rate of shipments will be 17%. However, the downward pressure on prices is huge and it drops by about 5% every year, so the annual growth rate of market revenue is 13%. In the consumer sector, there is also an interesting phenomenon: despite the wide application of combination sensors, discrete accelerometers still maintain the momentum of growth. Because wearable devices and the Internet of Things will also require a large number of discrete sensors. In addition, a Bosch discrete accelerometer was also used in the iPhone 6.

The combination of accelerometer + magnetometer sensors is suitable for feature phones, because they can use algorithms to simulate gyroscopes, thereby increasing the use of low-end mobile phones. The combination of 9-axis or 10-axis sensors will be driven by the growth of wearable devices.

We have also found many other MEMS device trends, such as the recent explosion of inkjet print heads for industrial applications, MEMS technology replacing the piezoelectric inkjet technology in the industrial and graphics markets, and replacing laser printing in the office sector. We also believe that the market for pressure sensors in smartphones, tablets, and wearables will exceed 580 million U.S. dollars in 2020. Another soaring market is consumer MEMS microphones. Medical, automotive and other applications are still in their infancy. In addition, micromirrors also have many industrial applications such as printing and forming, laser micromachining, photolithography, holographic data storage, spectroscopy, phototherapy, 3D measurement, microscopy, head-mounted displays, and network data centers.

The market for infrared microbolometers continues to grow, with 320 x 240 pixel resolution products gaining the most widespread use due to their good "resolution/cost" rates. It will still dominate because of demand from the automotive and surveillance markets. Although the launch of the Lepton module did not improve FLIR's 2014 performance, it and Seek Thermal (using Raytheon infrared imagers) will open up new markets for the future.

For RF applications, the bulk acoustic wave (BAW) filter market will be driven by high-end smartphones in the coming years. In the third quarter of 2014, Cavendish Kinetics released an impressive MEMS antenna tuning switch to meet the "reliability/cost" specifications of the consumer market.

Finally, we believe that chemical/gas sensors based on MEMS technology will become the future "star" products, and smart phones and wearable devices will be widely used.